At Anagram, we’ve spent many months thinking about, investing in, and building in the prediction market space. Much of our work has centered around a simple question: what kinds of new markets become possible when we can turn uncertain events into continuously priced distributions?

We’ve been exploring this extensively through our work with Acre. Here, the focus is on real estate, an economically enormous asset class that’s still subject to slow and fragmented pricing. Our goal has been two-fold: first, to let anyone forecast their views on real estate outcomes; second, to create a real-time price discovery platform that sophisticated participants can use to both derive pricing data and hedge their existing exposure. Building this required a new market-making design approach, in which our work with distribution markets became applicable.

Our work here led us inevitably to the insurance space. Put simply, we believe similar distribution market mechanisms are uniquely suited to the insurance use case, and we’ve recently been ideating on product angles for this.

Insurance is fundamentally about pricing uncertain future outcomes. Premiums represent the cost of trust and can be interpreted as a rent paid to an institution that prices, pools, collateralizes, and pays for this risk. In the context of blockchains, parametric insurance feels especially relevant because its structure is very compatible with programmable market infrastructure. Unlike the more familiar indemnity insurance, which pays after a claims adjustment process, parametric insurance pays when a predefined and measurable event occurs. If wind speed crosses a threshold, seismic activity reaches a specific magnitude in a region, or a fire crosses a geographical boundary, a payout is triggered, regardless of the actual insurable loss.

In the context of crypto, these clean triggers map naturally to verifiable oracles. Oracles map naturally to smart contracts. Smart contracts can make settlement deterministic. And under all of this, blockchains offer the global rails by which we can create new forms of financial products to share with the world.

This is the intersection between parametric insurance and onchain infrastructure that we’ve been exploring. At the heart of this is a broader question: can distribution market infrastructure create a new way to price, fund, and settle catastrophe risk, and what’s the wedge for a suite of products to exist in this domain?

A Primer on Parametric Insurance

One way to understand parametric insurance is that the loss adjustment for these contracts effectively happens upfront.

In more traditional indemnity insurance, the insurer evaluates a loss after the event. A policyholder files a claim, an adjuster assesses damage, the insurer interprets the policy, and payment follows if any portion of the loss is covered. While this is appropriate for situations where real damage occurs, the claims adjustment process itself is generally slow, subjective, and operationally heavy.

Parametric insurance (we’ll abbreviate this as PI going forward) moves much of this complexity to the design stage. The buyer, broker, and insurer agree in advance that a specific event will correspond to a specific payout. If the event happens under these terms, a payout follows, regardless of the magnitude of the financial loss. As a result, PI is fast, transparent, and objective. It can also cover risks that traditional policies may exclude, under-insure, or handle poorly. Case in point: business interruption, evacuation costs, lost income, high deductibles, supply chain disruption, and emergency operating expenses are all areas where speed and flexibility matter.

The largest tradeoff in a parametric system is basis risk. A parametric payout may not perfectly match the buyer’s actual loss. A buyer could receive a payout despite no damage, or suffer damage without receiving a payout because the trigger was not hit. This has historically been a central product tension and the reason PI has often been easier to sell to sophisticated commercial buyers than to ordinary consumers. Unknown to most, a large number of insurtech teams have innovated with novel parametric products aimed at the average insurance buyer, but few have gained significant adoption.

Zooming out, the rate of growth in the outstanding ~$22B PI market has accelerated noticeably over the last 18 months. This is largely due to an increase in perceived risk factors, including greater weather volatility, cyber concerns from AI, and an overall need to hedge longer-tail risks that traditional indemnity insurance won’t cover.

Airbnb recently rolled out parametric earnings protection for its hosts across 45 U.S. states, with payouts tied to external event triggers. And through a partnership with Sensible Weather, Booking.com offers a parametric weather guarantee that issues cash payouts if weather exceeds a stated threshold during your trip. Many other businesses across different industries are exploring unique risk coverage specific to their operations as well.

Catastrophe Risk and Capital Markets

The insurance industry essentially operates as a risk-transfer chain, designed to pass risk along to successive layers of intermediaries until it lands with those who have the broadest shoulders. In many cases, the broadest shoulders are found in the global capital markets.

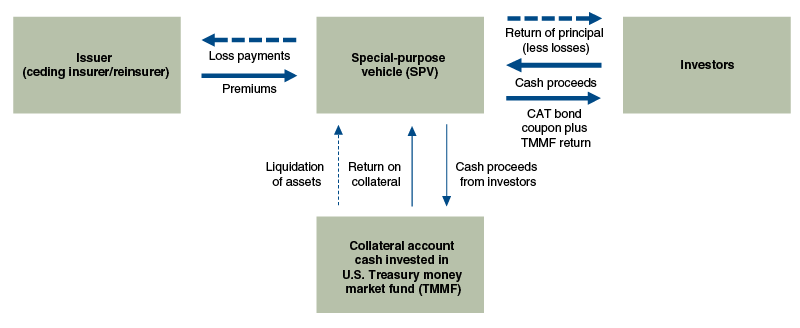

With natural catastrophes in particular, concentration risk is extremely high since a single hurricane, earthquake, or wildfire can generate thousands of correlated losses at once. This not only makes them especially challenging for traditional insurance underwriting, but also leaves exposed parties with large balance sheet risk from the policies they’ve extended. This is where catastrophe bonds (cat bonds) and other insurance-linked securities (ILS) become powerful. They provide a mechanism for insurers to transfer this peak disaster risk to the capital markets, while simultaneously allowing investors to earn uncorrelated market yield in exchange for bearing that risk.

Catastrophe Bond Structure (source: Chicago Fed)

The $66B cat bond market is almost exclusively institutional in nature and has high barriers to entry, effectively restricting access to sophisticated market participants. Transactions in these markets are typically structured via private placements, conducted as bilateral OTC deals, or structured through broker-to-broker contracts. This reflects the specialized modeling and capital requirements inherent in pricing and transferring peak disaster risk.

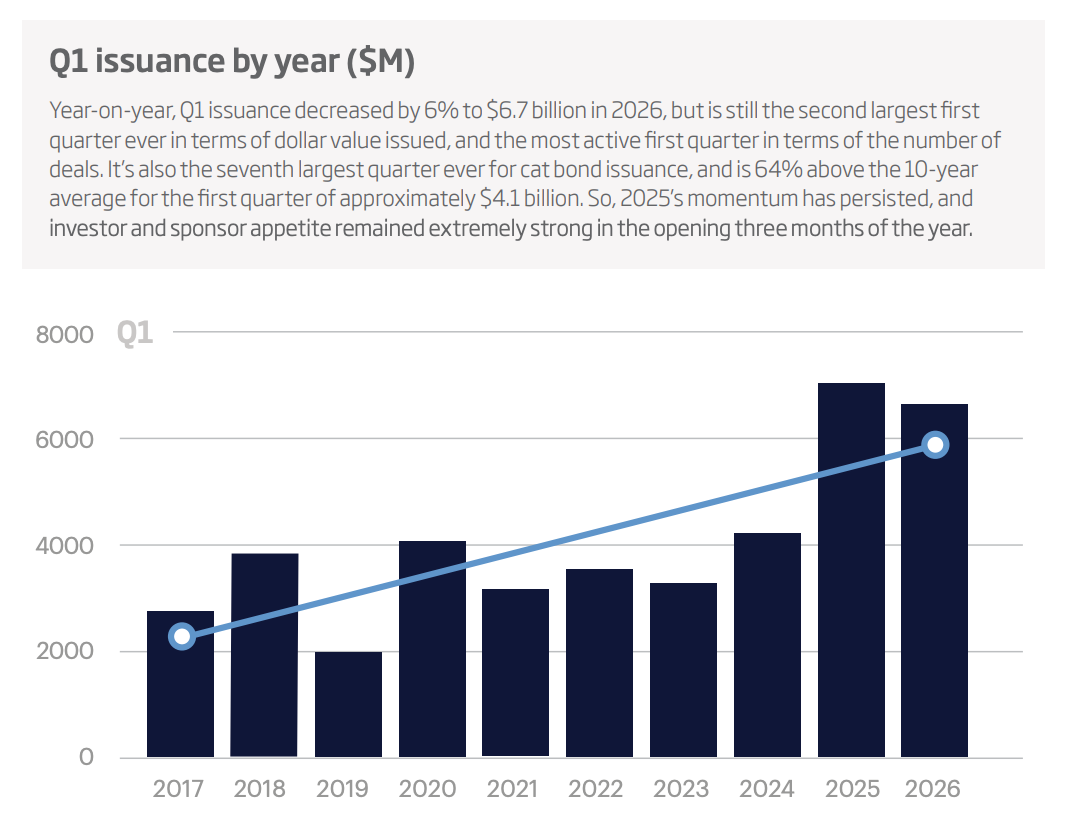

Q1’26 New Cat Bond Issuance (source: Artemis Market Report)

Of course, one of crypto’s most promising traits is its ability to democratize access to new financial markets on a global scale. We think this opportunity exists within the cat bond market as well.

Distribution Market Approach

Through our work with Acre, we saw clear parallels for applying our distribution market infrastructure to the world of insurance. Just as Acre can represent real estate outcomes as price buckets, catastrophe outcomes can be represented as probability buckets. For example, in the case of a hurricane event, the market might ask, “What wind speed bucket will this hurricane event fall into for this region and season?”

Buckets may look like the following:

1: Wind speed < 74 mph - no outcome

2: Wind speed 74-95 mph - Category 1 outcome

3: Wind speed 96-110 mph - Category 2 outcome

4: Wind speed 111-129 mph - Category 3 outcome

5: Wind speed 130-156 mph - Category 4 outcome

6: Wind speed 157+ mph - Category 5 outcome

By letting participants express views across this spectrum, the market can produce a live probability curve that reflects how expensive each part of the distribution has become. Insurance-like products can then theoretically be built as functions of this curve.

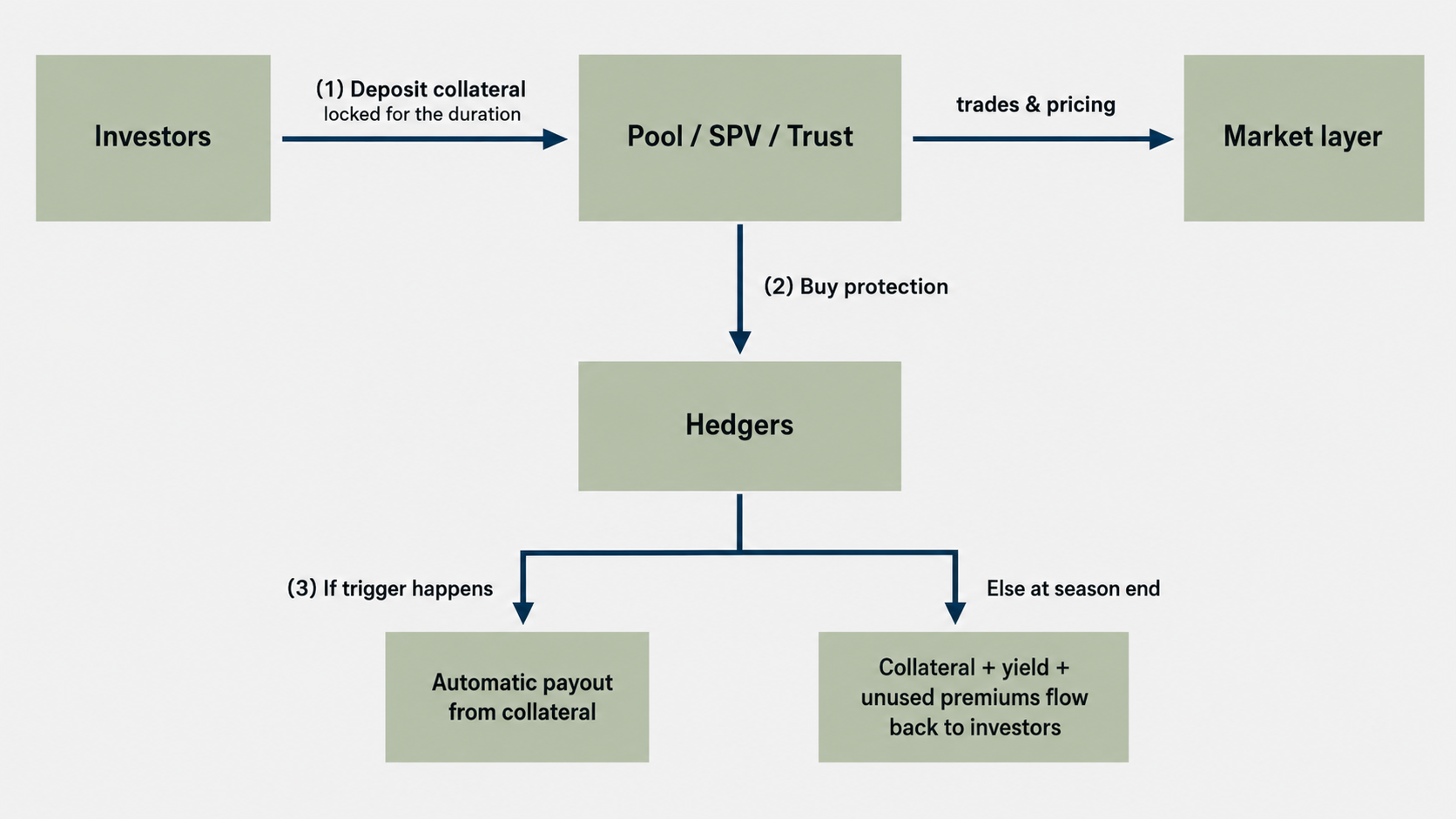

In short, a hedger (policy buyer) might buy protection that pays based on the event outcome. Investors/LPs might deposit collateral into an SPV pool to back these payouts, earning yield in the form of underlying treasury interest and the policy premiums in the case that no trigger event occurs.

For a simple flow –

Overview of Actors Involved:

• Hedgers/policyholders: homeowners, HOAs, municipalities, businesses, etc.

• Capital providers: investors supplying collateral to earn catastrophe risk premiums.

• Pool/SPV/trust: holds collateral and administers payouts.

• Oracle & calculation agent: computes the event outcome from defined data sources.

• Market layer: enables trading of standardized claims and investor pool shares.

Market Mechanics:

Overview of Market Mechanics (internal research)

Our engineering approach for this utilizes a Logarithmic Market Scoring Rule (LMSR) market-maker, an AMM originally used in prediction markets. We’ve adapted this into an LS-LMSR, which represents a liquidity-sensitive LMSR that automatically prices protection based on current demand, available LP collateral supporting this demand, and the amount of risk that has already been sold.

Importantly, the LS-LMSR replaces a fixed parameter with one that grows with market size. As more risk is bought/sold, the market naturally deepens, reducing slippage for large hedges. This is especially important when the market is used for real risk transfer at scale (millions in policy value) rather than small bets. In other words, early on in a risk season when the capital pool is smaller, there is more price movement per trade, which is healthy for price discovery. By contrast, late in the season when hedging flows are larger, the capital pool is deeper and there is less price movement per trade, which is good for stability.

Relative to more static actuarial models, a distribution-market approach makes the pricing logic more dynamic. It can reflect buyer demand, investor supply, perceived likelihood of different hurricane outcomes, and available collateral capacity at any given point. If many buyers want protection against severe hurricane outcomes, those outcomes become more expensive. If demand is lower or more collateral is available, pricing can adjust in the other direction.

This market structure ultimately reflects:

- Buyer demand

- Investor supply

- Relative likelihood of different hurricane outcomes

- Available collateral capacity

Importantly, the market stays solvent because the system tracks the maximum possible liability from all open policies. Before selling protection, it verifies that the liquidity pool has enough collateral capacity. The market will not extend more policies than it can pay out in the worst-case loss scenario.

Thoughts on Product and Form Factor

In scoping an MVP for this project, we decided to focus our initial efforts on the Florida hurricane insurance market. Florida has clear hurricane risk, high consumer awareness, expensive coverage (average premiums around $4k, $7k+ in coastal zones), large deductibles (typically 1-5% of insured value, 10% in high-risk zones), and an existing institutional market around hurricane exposure. Wind-speed triggers and storm categories are objectively measurable by an oracle source, and the market is large enough to matter but narrow enough to constrain an MVP.

Our first product concept has two sides. Consumers use a mobile app to buy hurricane-triggered cash protection with immediate payouts after a qualifying event. Investors seeking catastrophe-linked yield use a separate frontend to deposit capital into risk pools, earning interest in exchange for backing these policies. Depositors then have pool exposure that can be traded via a secondary market, though, importantly, not redeemed during the risk window. Investors can sell their pool share to someone else, but the collateral remains locked to maintain solvency in the system.

Our LS-LMSR mechanism sits in between these parties and translates market activity into a live pricing curve for hurricane risk. Through the market frontend, traders can take positions on risk outcomes, expressing their view on storm severity across these buckets. Their activity updates the relative price of each bucket, producing a market-derived view of the full distribution of possible hurricane outcomes. This distribution is then used to price the consumer protection policies being created against these markets.

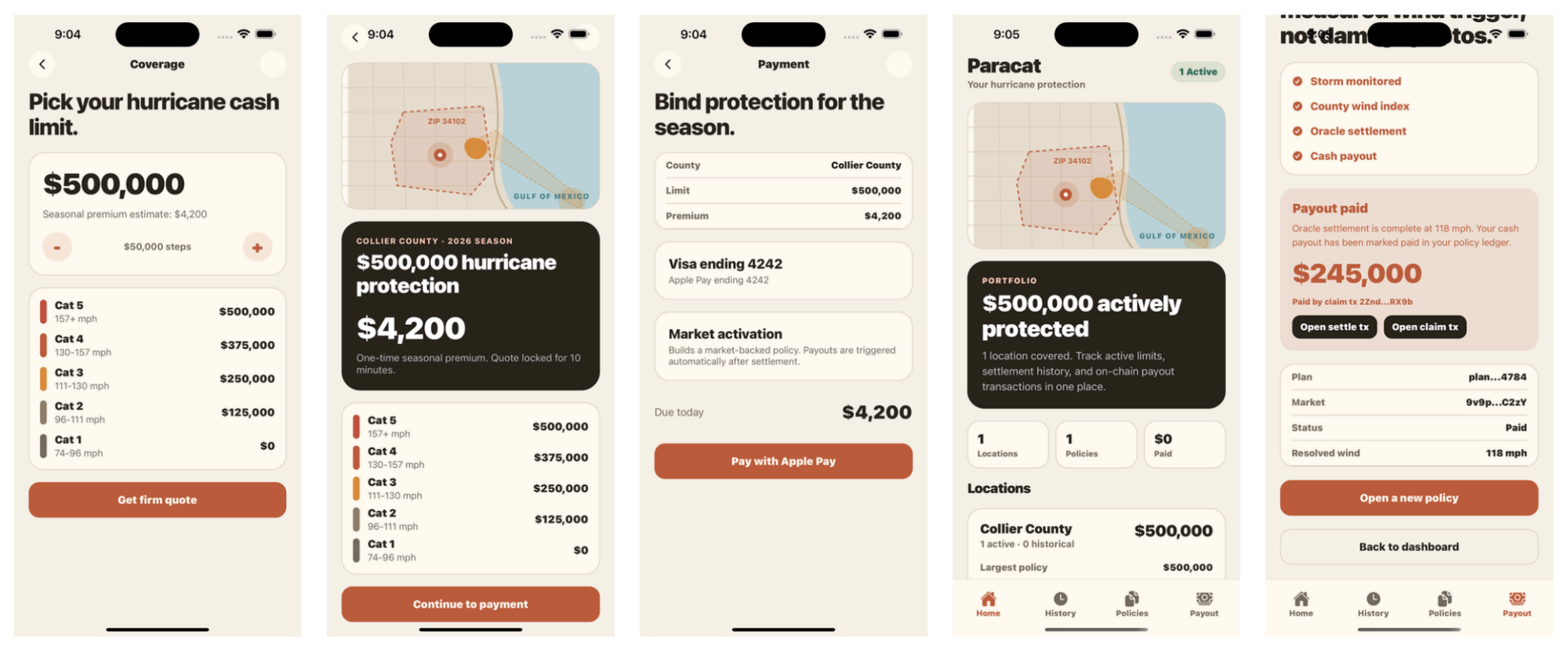

On the app side, the flow is intentionally simple: a homeowner enters their address to set the region, selects payout limits, reviews a tiered payout ladder by hurricane category, pays the premium, and then monitors their policy throughout its duration. If a trigger is hit, measured by the corresponding oracle sources, a payout is released automatically to their account. There is no claims adjuster process, no subjective loss assessment, and stablecoin infrastructure underpins the payment rails so there are zero banking delays.

Mock Consumer App (internal research)

This product is not meant to replace homeowners insurance, but in theory could sit next to it as a supplemental cash buffer to help cover deductibles, evacuation expenses, temporary repairs, hotels, cleanup, generators, power-loss costs, or any other immediate cash needs.

Still, our research and industry conversations have taught us that direct-to-consumer PI products are difficult. Many product attempts have failed to gain meaningful traction. Neptune Insurance ($3.8B) is the leader in private flood insurance in the U.S. with about 60% market share. The company acquired Jumpstart Insurance several years ago to offer its parametric earthquake product as an immediate cash supplement. This add-on hasn’t seen strong uptake, even when pitched in high-risk states like California.

Consumers tend to seek indemnity products because they want payouts tied to actual losses and admitted offerings with state guarantees, making customer acquisition here expensive. At the same time, buyers with the most meaningful property exposure generally work through agents, brokers, MGAs, or other intermediaries. It turns out that basis risk is uniquely challenging to grok, and even more difficult to sell.

To add to this, the consumers most likely to adopt a polished mobile insurance app skew younger and more digitally native, but this is the user cohort that often doesn’t own the highest-value property exposure in the first place. Meanwhile, those with the most acute insurance pains (coastal homeowners, HNW property owners, HOAs, condo associations, commercial property operators) tend to rely on agents, brokers, boards, advisors, and other trusted intermediaries in this process.

For this reason, we’re also exploring a potential B2B2C distribution model built around relationships with channel partners. The form factor in this case might be a bundled offering where a supplemental parametric product is offered together with traditional indemnity insurance through brokers, MGAs, mortgage platforms, or specialty insurance distributors.

One compelling version of this might be a deductible buffer. A homeowner facing a very expensive hurricane policy might choose a higher-deductible plan to reduce their annual premium, then purchase a parametric product to offset part of that deductible exposure if a storm occurs. The value prop to a selling agent here is that such a product might increase the ease with which they can sell higher-deductible policies rather than losing customers to churn.

Of course, closing partnerships with these agents is a feat on its own, one that requires real legwork and boots-on-the-ground sales motion. With its own parametric offerings, even Neptune is forced to run manual distribution in many situations, hiring reps to visit local agents in person to sell at these distribution points. In today’s digital world, the insurance industry still requires humans with donuts.

Example Product Distribution Strategies (internal research)

In addition to the consumer scope, our research in this area also covers an institutional build. Clearly, the more durable business may not be a standalone consumer app itself, but the infrastructure behind it: pricing, collateral, monitoring, settlement, reporting, and data. This is a longer-term vision, but one we believe has potential.

An institutional product would look less like an app and more like a catastrophe-risk platform. Protection buyers (insurers, MGAs, brokers, municipalities, HOAs, property managers, etc.) need a way to structure and purchase parametric hurricane protection. Depositors (ILS funds, reinsurers, family offices, and other capital providers) need a way to allocate collateral into defined risk pools and understand the exposure they’re taking.

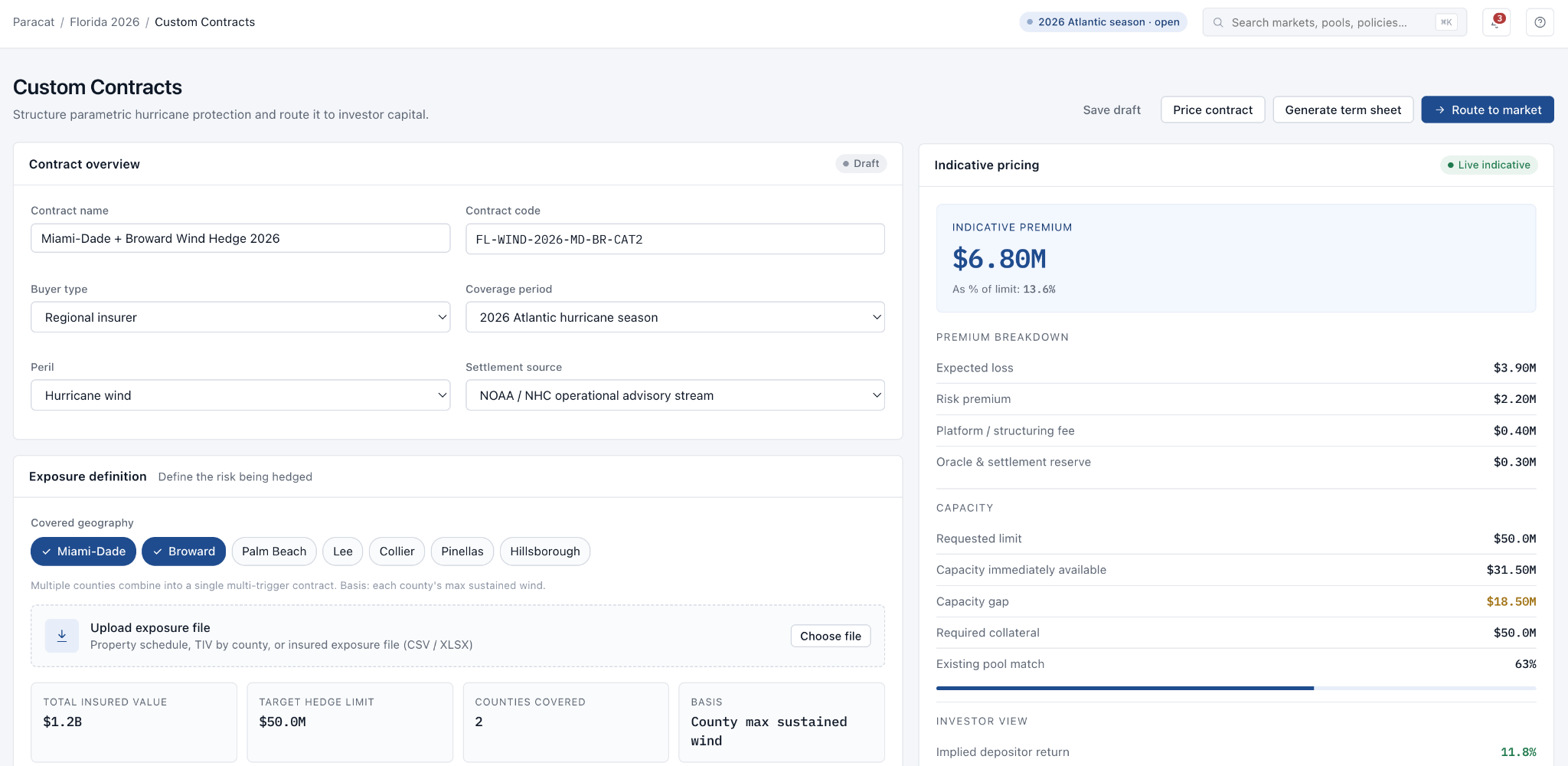

A platform could connect these two groups around hurricane severity markets. A buyer might use it to purchase a standardized contract, such as Cat 3+ protection for a single county, or structure a bespoke multi-county hedge. Or perhaps there’s a custom contract builder where buyers can define a custom protection contract specific to their exposure. That contract could then be matched against existing pool capacity, sent to a private auction for investors to take the other side (similar to OTC cat bond transactions), or routed to an open marketplace in the form of an order book.

Mock Custom Risk Contract Builder (internal research)

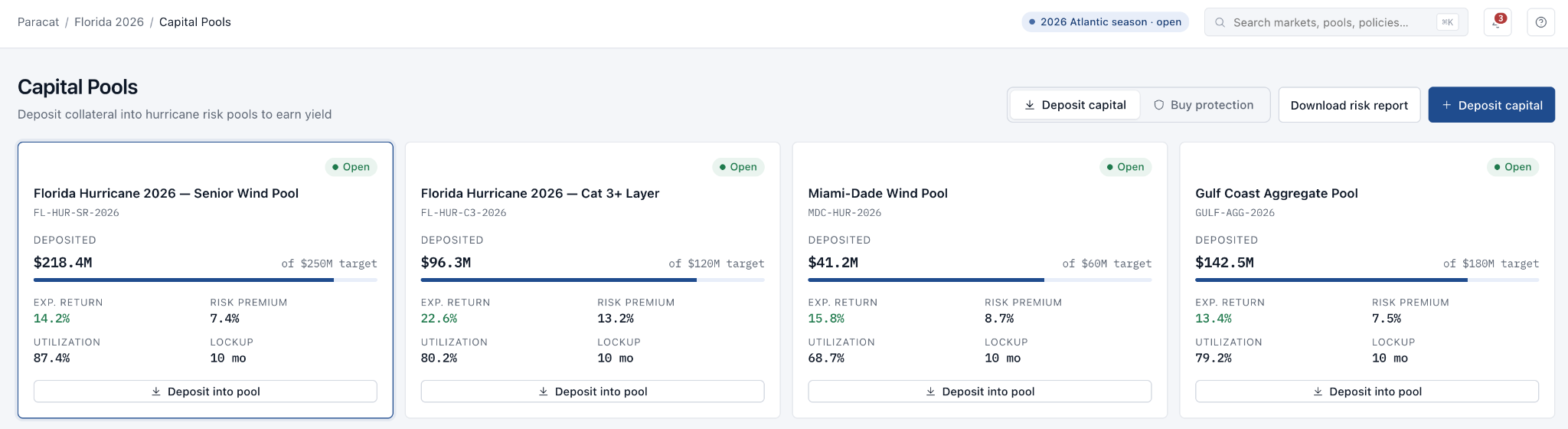

For depositors (investors), the platform might feel more like a portfolio dashboard. A capital provider could review available pools, expected return, risk premium, utilization, lockup period, any backtests or stress scenario data, exposure by county, and other relevant metrics. Once they’ve deposited into a pool, they could monitor their capital at risk, earned premium/yield on their collateral, mark-to-market value, and real-time storm exposure.

Mock Depositor Dashboard (internal research)

This platform might also have an operational layer. A live storm monitor could track active events and forecast trigger probabilities. The oracle system could display live readings, ingest official NOAA or NWS wind data, determine when triggers are hit, initiate the settlement engine for onchain payouts, and produce institutional audit reports – all fully verifiable onchain.

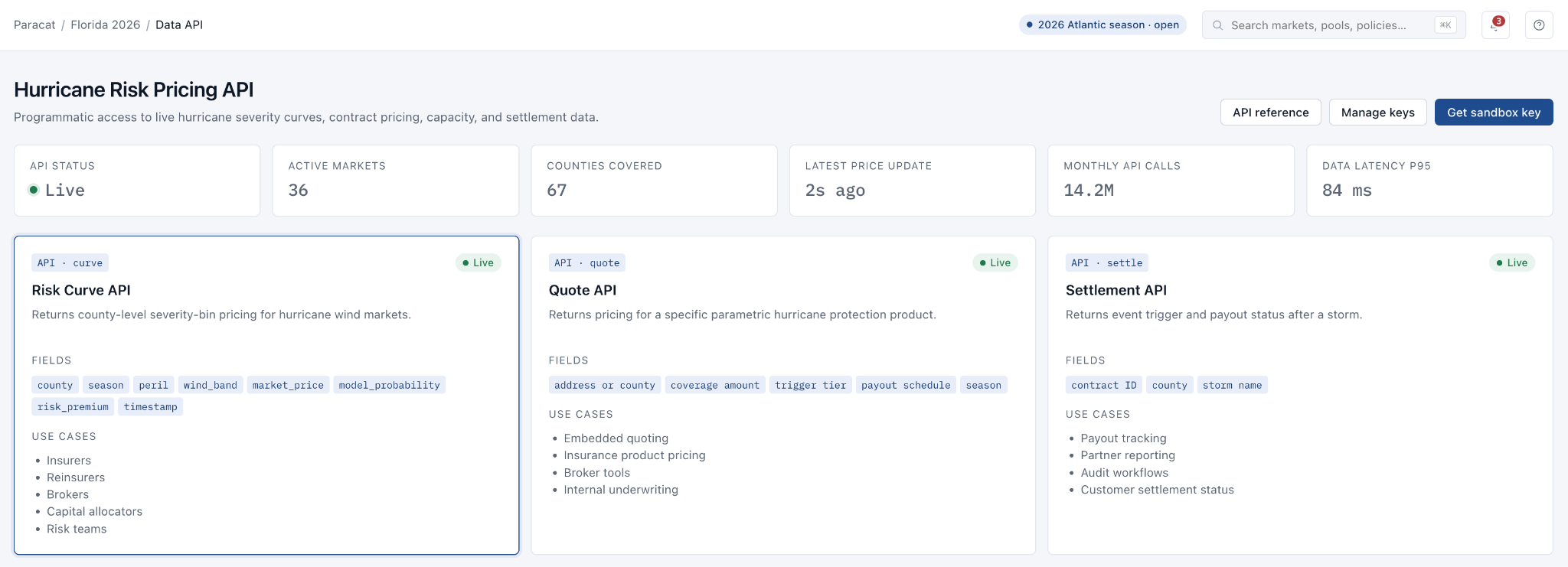

A data API alone could also become a full product from this infrastructure, exposing risk data, policy quotes, settlement status, and market depth to institutional users who don’t need a full UI.

Mock Data API Product (internal research)

Like any market, these products are heavily constrained by liquidity and participating capital. This is no different from binary prediction market platforms today. The product form factors introduced above are simply conceptual ideas, and each becomes useful only if the market around it is deep enough to support real risk transfer.

So the point is not that this structure immediately replaces insurance, cat bonds, or reinsurance. It does not. The point is that parametric risk may be unusually well suited to market-based infrastructure because the product already relies on defined triggers, objective data, and known payouts. If distribution markets can help price these risks more dynamically, and onchain systems can help collateralize and settle them more transparently, and crypto rails can extend these markets globally, then there may be a new design space worth exploring.

Insuring the Long Tail

Thinking more broadly, the best wedges for building truly sticky parametric products may actually be in the long-tail risks that traditional insurance handles poorly. New infrastructure to remove friction and reduce costs in the traditional insurance industry is a nice selling point, but business opportunities based only on rent compression often get eroded by regulation, thin margins, legacy adoption, non-blockchain competitors, or lack of new enablement. “Cheaper insurance onchain” may not be durable by itself.

A stronger thesis here pairs cost compression with new capabilities: covering risks that legacy carriers cannot serve well, settling instantly, reaching excluded markets, or creating new risk markets altogether.

Possible markets here include those where the buyer has a clear operational exposure, the trigger is measurable, and the payout solves a real liquidity problem. Hail risk for car dealerships is one niche example we've socialized. A dealer may have hundreds of vehicles sitting exposed on a lot, and a hail event can create immediate working-capital strain from damage. Snowfall risk for ski resorts and their customers is another: poor snow conditions can directly affect bookings, staffing, and operating revenue. As an individual, I might similarly be interested in purchasing protection related to snow conditions if I’m planning on taking an expensive ski trip.

There are many niche long-tail risks that PI products might uniquely address. Some fun ones we can think of:

- Outdoor event weather protection – Payouts for weddings, festivals, sports tournaments, concerts, and conferences might be tied to rain, heat, wind, or air quality thresholds.

- Power outage protection for households and small businesses – Payout if a grid outage exceeds a defined duration in a service territory.

- Solar irradiance protection – Payout if sunlight & production conditions fall below modeled thresholds for solar farms, solar projects, or community solar operators.

- Data center SLA protection – Payout if cooling-related environmental conditions threaten uptime commitments.

- Robot fleet downtime protection – Payout if a verified fleet-management system shows a robot fleet is offline or below operating capacity for a defined period.

- Launch delay protection – Payout if a spacecraft launch is delayed beyond a defined window due to vehicle readiness, regulatory hold, launch-provider scrub, weather, range availability, or other factors.

Get In Touch With Us

Our work here is still early.

The insurance industry has many hard problems to solve, and parametric insurance in particular has had many false starts. The mechanism is compelling, but the product only matters if buyers understand it, distributors can sell it, and capital is willing to stand behind it.

That said, we think the intersection here between distribution markets and new methods of risk transfer is worth continuing to explore. We’re actively learning from insurance operators, brokers, ILS investors, and crypto-native builders.

If you’re building in this area, investing in it, underwriting these risks, distributing insurance products, or simply thinking about how real-world risk markets might evolve, we would love to compare notes.

References

- Anagram Research Whitepaper: “Catastrophe Insurance & Cat Bonds on Prediction-Market Rails”

- FT Partners: InsurTech May 2026 Market Update

- Gallagher Re: Global InsurTech Report (May 2026)

- Artemis: Q1 2026 Catastrophe Bond & ILS Market Report

- Federal Reserve Bank of Chicago: “Catastrophe Bonds: A Primer and Retrospective”

- 1kx: “Cost of Trust 2.0”

- Insurance Insider: “From Niche Tool to Core Option: How Parametric Covers are Maturing Fast”

- Discussions with MS Transverse Insurance Group

Legal Disclaimer

The information in this article has been prepared by Anagram Ltd. (“Anagram”) for educational and informational purposes only. Under no circumstances should this, or any post on this website, be construed as solicitation for investment in Anagram, its affiliates, or any projects named herein or otherwise. The contents herein, and content available on any associated distribution platforms, including Anagram online social media accounts, should not be construed as or relied upon as investment, legal, tax, or other advice. Certain information contained herein, including in charts and graphics, may have been obtained from third parties. While such sources are believed to be reliable, Anagram does not assume any responsibility for the accuracy or completeness of such information. No assurance is made by Anagram regarding the accuracy or completeness of the information or opinions set forth herein, whether or not obtained from third parties, and Anagram shall not be liable therefor. Certain statements herein are based on subjective beliefs, may differ from the views of other market participants, and are subject to change. This presentation contains “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may”, “will”, “should”, “expect”, “anticipate”, “project”, “estimate”, “intend”, “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially and adversely from those reflected or contemplated in the forward-looking statements. Anagram and its affiliates may consult, invest, build, or otherwise have interest in companies or projects that are written about in this space. This content is for educational purposes only and does not constitute advice, marketing or solicitation for funding.